If we take a look at the Bitcoin price chart, it’s quite easy to picture the ever-growing number of investors who, since the cryptocurrency’s first peak in June 2016, have found themselves spending one or more nights staring at those green and red lines, studying spikes and dips, desperately searching for a pattern that would help them predict the currency’s future value. Is it ever possible to predict the value of a cryptocurrency? How about the value of an NFT?

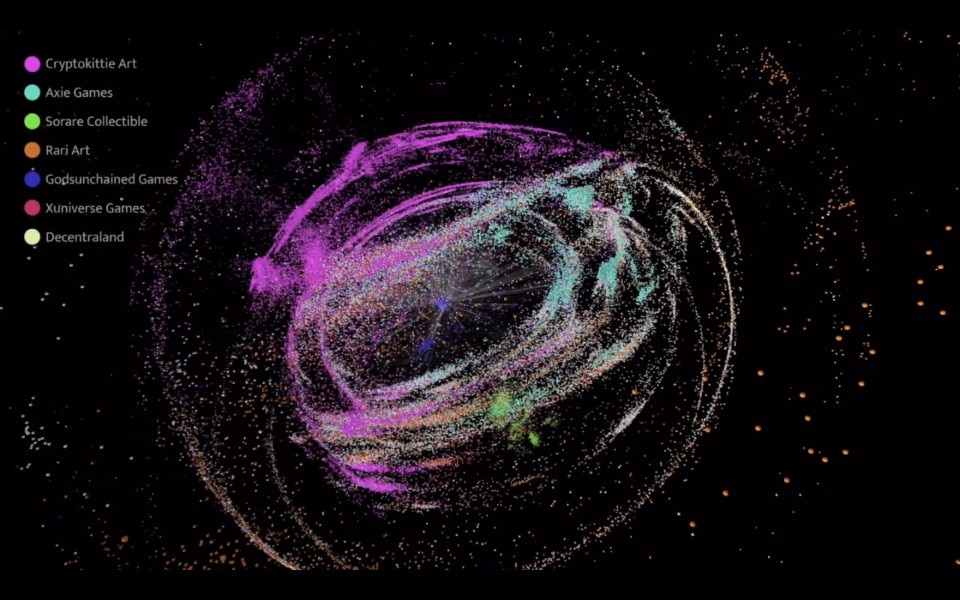

In March 2021, following the worldwide news that the NFT associated with the work of art by US artist Beeple Everydays: the First 5000 Days had just been sold by Christie’s for almost 40,000 Ether, corresponding to $69.3 million at the time of sale, researchers at the Alan Turing Institute decided to set up a data collection and analysis system that would tell the story of the NFT market from June 2017 to April 2021, covering a total of 6.1 million transactions. The recently published article Mapping the NFT revolution: market trends, trade networks, and visual features attempts to identify which factors determine the selling price of an NFT.

In just one year, the non-fungible tokens (NFTs) market has grown from around $340 million to $14 billion, and while some people are still questioning the point of investing in a .jpg and others are protesting against the environmental impact of proof-of-work transactions, luxury brands and auction houses, from Gucci to Sotheby’s, are rushing to launch their metaverse – a series of virtual places where it is now possible, among other things, to collect avatars and game items, wear digital designer clothes and exhibit intangible works of art, all easily purchased in the form of NFTs. In this new market, art and fashion come surprisingly second, imitating and seeking collaborations with the video game industry, while Morgan Stanley claims that in less than ten years, 10% of the luxury industry will be made up of NFTs bought, purchased and above all – get this! – rented, in the metaverse.

These staggering numbers raise further doubts and questions: Is this a bubble destined to get bigger and bigger as long as there are newcomers, and then to finally pop, or is it an investment capable of securing forms of “eternal passive income”, especially when NFTs can be rented out? From a conversation with two of the authors of Mapping the NFT revolution, some questions were finally answered.

Mauro Martino, director of the Visual Artificial Intelligence Lab at the MIT-IBM Research AI Lab in Cambridge, and Andrea Baronchelli, head of the Economic Data Science team at the Alan Turing Institute, tell us how from the very beginning – that is, since the rise of CryptoKitties (2017), one of the very first successful experiences in the world of NFTs – what we will call the first secret of the value of NFTs was already very clear: the sale value of NFTs depends on the community that supports them.

Martino notices how the sentence of having to be recognisable, the nightmare of every artist and the imposition of every art gallery, is also present in the NFT industry.

Here we are at the dawn of a new digital age. While we ask ourselves whether it makes more sense to invest in a sweatshirt made of only pixels from the “Balenciaga x Fortnite” collection, or in a piece of land next to rapper Snoop Dogg’s villa on the Sandbox metaverse, or simply in a digital potato, like the one sold by Irish artist David OReilly on the website of Japanese auction house SBI Art Auction, we should look, first of all, more than at the object for sale, at the potential fan base that supports it.

According to the researchers, this leads us to discover the “second big secret” of the sales value of NFTs: communities and capital are more likely to nest around collections or gamified experiences than episodic sales.

In Mapping the NFT revolution we discover that the greatest NFT buyers, the so-called whales, aren’t a lot – “the top 10% of traders alone make 85% of all transactions” – and tend to get attached to a single collection, making “at least 73% of their transactions in their main collection”. It is hardly surprising that companies traditionally associated with the world of sticker and card collecting, such as the NBA, MotoGP, Panini or Magic the Gathering, have jumped into the fray, quickly creating their own digital marketplaces.

As Martino and Baronchelli explain, the NFT landscape varies greatly depending on the industry it belongs to. There is the art world, where newly formed crypto marketplaces such as Foundation, Rarible and Nifty Gatheway fight against traditional auction houses. There are NFTs belonging to the “Metaverse” category, which would make no sense to exist outside of that world, as well as NFTs generated by the “Gaming” industry. Finally, there is the “Collectibles” category, the virtual counterpart of collectible cards, which could be considered as a kind of progenitor to imitate.

In Mapping the NFT revolution’s prediction system, half of which is based on data from previous sales, a big variable is the visual appearance of NFTs, analysed using AlexNet, a pre-trained convolutional neural network, which is simply an artificial intelligence that can ‘see’ images and detect recurring patterns. And what it sees is that buyers seem to like similar images. Just like the most mundane textbook instruction in social media management, the consistency of the feed rewards the artist.

Martino notices how the sentence of having to be recognisable, the nightmare of every artist and the imposition of every art gallery, is also present in the NFT industry: if Basquiat was forced to be Basquiat, today Mad Dog Jones will be permanently bound to the bright colours of post-vaporwave and to the cyberpunk illustrations that make him Mad Dog Jones, one of the most famous and prolific NFT artists on the scene. Apparently, as Martino and Baronchelli laughingly observe, even the non-fungible token, to sell better, ends up becoming fungible, i.e. potentially replaceable by a series of works that are identical to themselves.

Speaking of artists, here is the “third big secret” of the value of NFTs: the art market is an entirely secondary aspect of the NFT phenomenon. As of June 2020, “the most traded NFTs belong to the games and collectibles categories. Only 10% of transactions are related to the NFTs classified as art”.

We are dealing with a complex technology in its first years of use. We can imagine it, the researchers explain, as a Lego tower with vaults and architraves that the most diverse market forms are trying to mount on top of their castles, or their galleons, or their Lego spaceships. Infrastructures that are juxtaposed with other infrastructures, only to undergo violent processes of adaptation, including collapses, breakdowns and work fatalities.

The art market is an entirely secondary aspect of the NFT phenomenon.

In this scenario, the art industry is perhaps finding it most difficult to adapt. Attempts to gamify works or create communities around collections seem more forced than ever. And if we look at the success stories from the period of the so-called “NFT Craze” between February and June 2021, the greatest sales were made possible by unique factors that are difficult to repeat: “the first NFT sold by a traditional auction house”, i.e. Beeple, “the first Tweet”, i.e. Jack Dorsey, “the first NFT meme” i.e. Nyan Cat, or “the most famous meme ever” as well as the most iconic figure in the crypto world, i.e. Doge, or indeed one of the few visually and technically coherent digital art collections: Art Blocks.

Who guarantees that so many of the NFTs bought during this period of madness will be resold a second or third time, one, three, ten years from now? So far, the data do not look good: out of 6.1 million transactions, only 20% of NFTs were resold a second time, as Martino and Baronchelli note.

And so, we come to the end of this umpteenth gamification attempt, and thus to the fourth and last “secret”: it is impossible to imagine what the value of current NFTs will be one year from now, let alone in ten years from now, given the speed and the massive amount of works, tokens, platforms and metaverses that are currently on the table.

Remember the dot-com bubble at the end of the 1990s? This is a phenomenon of equal size and greater complexity, the researchers explain. We can assume that, as with dot-coms, when hundreds or thousands of economic proposals proliferate, only a few giants will survive, crushing and absorbing their competitors. In the transition between Web 2.0 and Web 3.0, as Baronchelli suggests, it is possible that the current economic system, where the user participates by enjoying free content while donating his data to a centralised platform that reaps huge profits, will be replaced by a model where the concept of ownership is redistributed among users. Following an observation by Matthew Ball, an acclaimed theorist of the future metaverse: if it wasn’t the New York Times, or any other print media mogul, that developed the most used news feed in the world – *spoiler* it was Facebook –, it will probably not be Facebook Meta that will develop the most frequented metaverse, or who knows what it will be called in three years, the most frequented tokenized virtual space.

Opening image: Machine Hallucinations – Space: Metaverse NFT Collection, Refik Anadol, Sotheby’s, 2021